Yesterday we discovered something surprising. It is possible to send money to someone on the internet without a bank acting as the middleman. Instead of relying on a financial institution to verify and record the transaction, Bitcoin uses a global network of computers that collectively maintain a shared ledger called the blockchain.

But that raises an obvious question.

When you send Bitcoin to someone, where does the transaction actually go?

If you send money through a bank, the answer is simple. The bank updates its internal database. Your balance decreases, the receiver’s balance increases, and the bank stores that information on its servers.

Bitcoin works very differently.

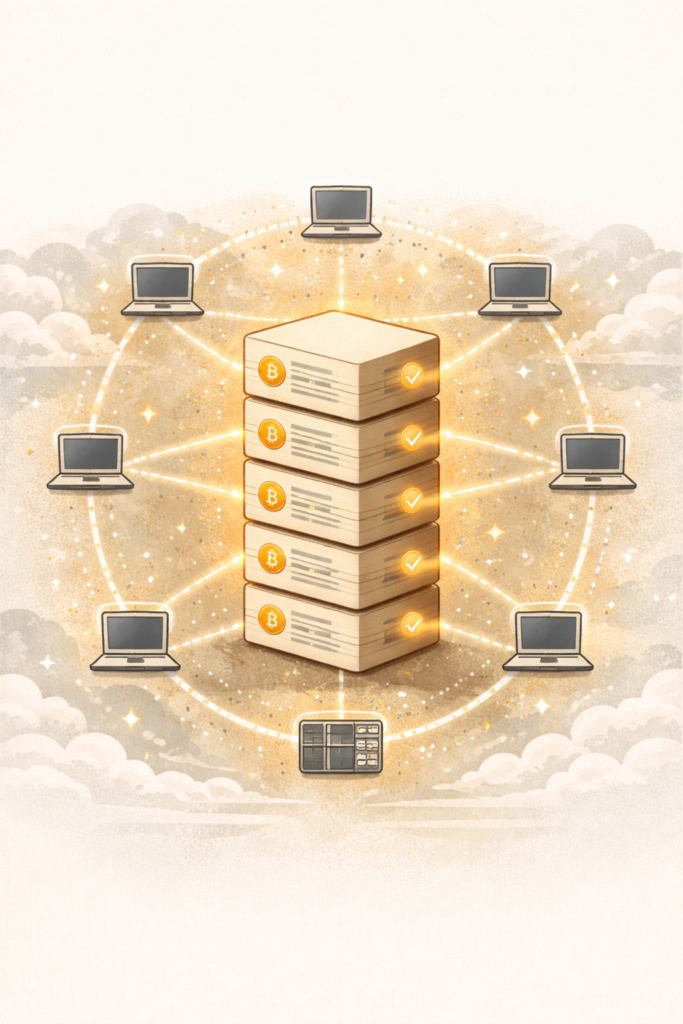

When you send Bitcoin, the transaction is not stored in a single company’s database. Instead, it is broadcast to thousands of computers around the world that are part of the Bitcoin network. These computers are constantly communicating with each other, sharing information about transactions and maintaining a synchronized record of what has happened on the network.

To understand this idea more easily, imagine a giant Google Sheet that records every Bitcoin transaction ever made. Anyone can see it, and thousands of computers keep their own copy of it. Whenever a new transaction happens, that transaction is added to the sheet and everyone updates their copy.

So when you send Bitcoin to Rahul, the transaction is essentially announced to the entire network. The network then records it in this shared global ledger.

This ledger is what we call the blockchain.

The word blockchain sounds complicated, but the idea behind it is actually quite simple. It is just a long chain of records, where each record contains a group of transactions. These groups of transactions are called blocks. Once a block is filled with transactions, it is added to the chain of previous blocks. That is why the system is called a blockchain: blocks of transactions linked together in chronological order.

You can think of each block like a page in a notebook. Every page contains a list of transactions that happened during a certain time period. When the page is full, it is sealed and a new page begins. Over time, these pages form a complete history of everything that has happened on the network.

What makes this system special is that once a block is added to the chain, it becomes extremely difficult to change. If someone tried to alter an old transaction, they would also have to modify every block that came after it, and they would have to do it across thousands of computers at the same time. That level of coordination is practically impossible, which is why the blockchain is considered highly secure.

Another interesting aspect of the blockchain is that it is completely transparent. Anyone in the world can look at the Bitcoin blockchain and see all the transactions that have ever occurred. Of course, the identities of the people involved are not directly visible. Instead, transactions are associated with wallet addresses, which appear as long strings of characters.

This means the system is open and verifiable, yet still preserves a certain level of privacy.

If we compare this to the traditional banking system, the difference becomes very clear. Bank databases are private. Only the bank has access to them, and you must trust the bank to maintain the records correctly. In contrast, the blockchain is public. The records are shared across the entire network, and anyone can verify them independently.

This design removes the need for a central authority to maintain trust. Instead of trusting a bank, users trust the transparency and security of the system itself.

But there is still an important piece missing from the story.

If transactions are broadcast to the network and stored in blocks, who decides which transactions get added to the blockchain? Who organizes these blocks and links them together?

This is where a special group of participants comes into play.

They are called miners.

Miners play a crucial role in maintaining the Bitcoin network. They collect transactions, verify them, and package them into blocks that become part of the blockchain. In return for doing this work, they receive newly created Bitcoin as a reward.

In the next post, we will explore how Bitcoin miners operate, why they compete with each other, and how their work keeps the entire network secure.

Once you understand mining, the inner workings of Bitcoin will start to become much clearer.